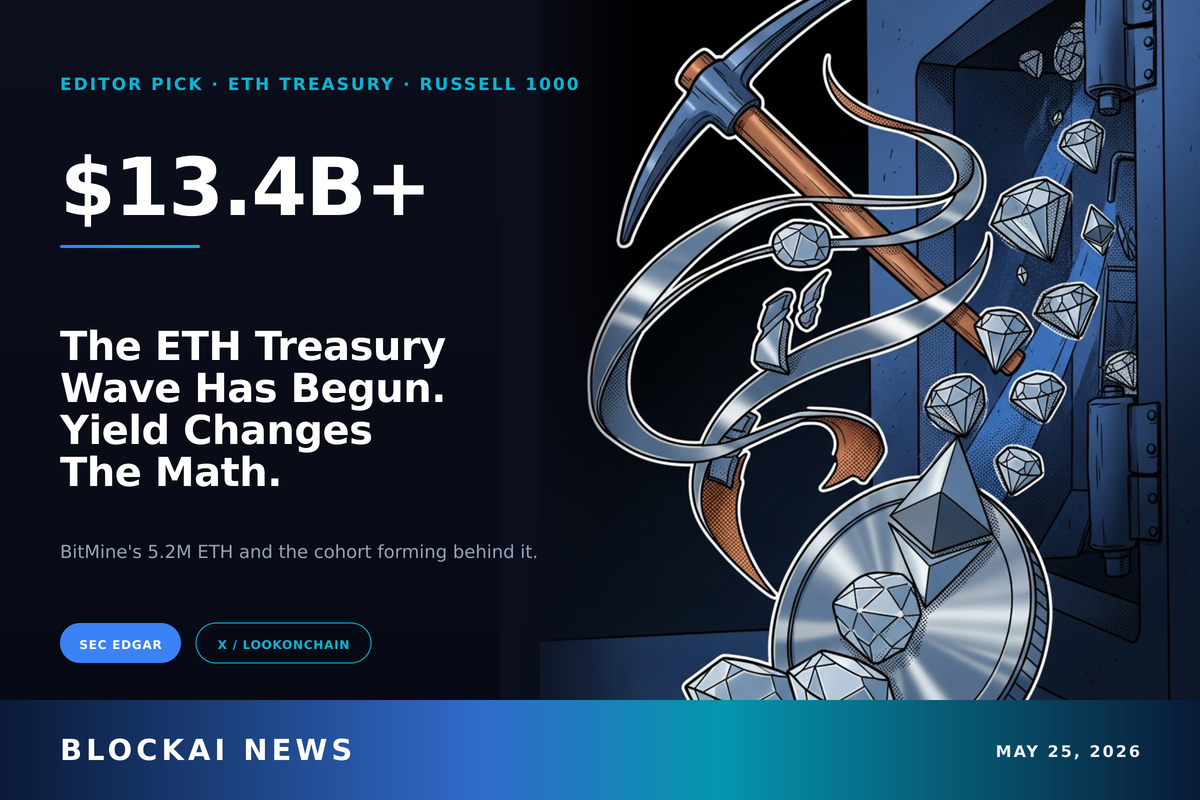

The ETH Corporate Treasury Wave Has Begun — And Yield Changes the Math

BitMine's 5.2M ETH stack is not a one-off. With SBET, BTCS and Bit Digital behind it and Russell 1000 inclusion looming, an ETH treasury cohort is forming. The difference from the BTC playbook: staking yield turns the equity into something that looks like a cash-flow multiple.

On May 23, Tom Lee's BitMine Immersion Technologies bought another 60,000 ETH for roughly $126 million, lifted its treasury to more than 5.2 million ETH — about 4.37% of all circulating Ethereum — and got named to the preliminary Russell 1000 inclusion list in the same week. Read together, those three lines mark the moment the ETH corporate treasury thesis stopped being a single-name BMNR trade and started looking like a cohort. SharpLink Gaming sits behind it with roughly 867K ETH and an in-house staking desk. BTCS Inc. and Bit Digital hold smaller but operationally serious positions. A queue of private-round vehicles is forming. The 2024-25 MicroStrategy BTC treasury wave had Michael Saylor's religion. The 2026 ETH treasury wave has a 2.9% staking yield curve — and that changes the math.

TL;DR

- BitMine's 5.2M+ ETH treasury and its $126M May 23 buy is no longer a one-off — SharpLink Gaming (~867K ETH), BTCS (~70K ETH), and Bit Digital (~155K ETH) form a real cohort, with private-round vehicles queueing behind them.

- The defining difference from the BTC treasury playbook: ETH stakes. BitMine has roughly 4.36M ETH staked; protocol-native yield around 2.9% annualized gives the equity premium something resembling a cash-flow multiple — not just a directional bet.

- Russell 1000 fast-entry (BMNR's preliminary inclusion, final reconstitution in June 2026) creates a forced passive-buyer regime early MicroStrategy never had — but with average cost basis near $4,000 and ETH near $2,100, the flywheel is one NAV-premium compression away from stalling.

How BitMine Made the "MicroStrategy of ETH" Real

A year ago, the phrase "MicroStrategy of Ethereum" was a Twitter joke. Two years ago it was a thought experiment in a Fundstrat note. As of this week, it is a 10-Q footnote, a Russell preliminary list entry, and a daily PRNewswire ritual.

BitMine Immersion Technologies (NYSE: BMNR) disclosed a treasury that has now crossed 5.21 million ETH and $13.4 billion of total crypto and cash. Of that, the company reports roughly 4.36 million ETH staked and generating protocol-native rewards. The cadence is not subtle: BitMine has been buying in chunks of 60K-100K ETH per week through most of 2026, frequently announcing it via PRNewswire the same day. The May 23 buy of about 60,000 ETH for $126 million was the latest installment.

The mechanism is the same one Michael Saylor wrote into the playbook in 2024. BitMine issues equity at a premium to net asset value via at-the-market programs. It deploys those proceeds straight into ETH. ETH per share goes up. Sentiment compounds. The premium widens. Issue more equity. Buy more ETH. The reflexivity Tom Lee, BitMine's chairman, openly described on X — "increasing ETH held per share and also driving reflexive benefits by accumulating a larger share of the supply of ETH" — is the engine.

What is different about BitMine is that the engine has been pointed at a productive asset from day one. BitMine's 8-K disclosures separate staked and unstaked ETH balances. The staked balance is not a footnote. It is the thesis.

The Yield Multiplier: Why ETH Treasuries Are Not BTC Treasuries

This is where the analogy with MicroStrategy's BTC strategy breaks, and where the 2026 ETH treasury wave starts to deserve its own valuation framework.

A Bitcoin treasury holds a non-yielding bearer asset. The entire bull case for an MSTR-style vehicle is directional: BTC appreciates faster than the dilution and debt service. There is no recurring economic flow to discount. There is faith, leverage, and a chart.

An ETH treasury holds a yield-bearing asset. According to Bit Digital's own March 2026 disclosure, its staked ETH generated approximately 291.3 ETH in rewards in a single month, working out to an annualized yield of roughly 2.9%. Network-wide reference rates from third-party indexes sit in a similar 2.9-3.3% band depending on validator mix. Apply that to BitMine's roughly 4.36 million staked ETH and the implied annualized in-kind yield runs near $290 million worth of ETH at today's price — a non-trivial number against a $13.4 billion balance sheet.

2024 BTC treasury was religion. 2026 ETH treasury is math — because for the first time, the equity premium has something that smells like a cash flow underneath it.

That changes how a serious equity analyst can build the model. It is no longer purely premium-to-NAV. It is premium-to-NAV plus a recurring in-kind yield that compounds the ETH stack itself. The yield is not a fee, it is not a loan, it is not a hedged carry. It is the protocol minting new ETH directly into the corporate treasury for performing validator work. That is a categorically different asset to underwrite.

Tom Lee (@fundstrat) breaks down why BitMine chose ethereum as its treasury asset.

— Pantera Capital (@PanteraCapital) July 11, 2025

"Treasury Secretary Bessent thinks it [stablecoins] could be a $2T market. From $200B today, that's 10 times growth. That's exponential. That would create exponential demand for Ethereum.” pic.twitter.com/uliSafsUN1

Pantera Capital, surfacing Tom Lee's framing on X (see @fundstrat), captured the macro overlay neatly: if stablecoin supply scales from roughly $200B today toward Treasury Secretary Bessent's stated $2T target, the resulting fee flow and settlement activity feeds directly into ETH demand. An ETH treasury company is, in that framing, a leveraged play on stablecoin adoption with a staking coupon attached. There is no equivalent narrative for a BTC treasury.

The Cohort Forming Behind BMNR

One company is a story. A cohort is a regime. The cohort is now visible.

SharpLink Gaming (NASDAQ: SBET) is the second-largest disclosed corporate ETH treasury. The company's February 2026 8-K reported aggregate ETH holdings of 867,798 — split across native ETH, liquid-staked ETH and wrapped liquid-staked ETH — and 13,615 ETH of cumulative staking rewards since launching its strategy in mid-2025. In April 2026, SharpLink terminated its outside managers ParaFi Capital and Galaxy Digital and moved treasury operations fully in-house. That is not a balance sheet decision. That is a company telling its shareholders it intends to run a full validator and staking operation as a core competency.

BTCS Inc. — which has been an Ethereum-focused validator and block-builder for years — held more than 70,000 ETH as of early 2026, paid an in-kind ETH dividend to shareholders (an unusual structural choice that essentially says "the staking yield is real, here, have some"), and runs the operation as a vertically integrated network infrastructure business rather than a passive holding vehicle.

Bit Digital (NASDAQ: BTBT) has rebranded itself as a "Strategic Asset Company" with ETH and AI-compute exposure. Roughly 155,000 ETH as of late Q1 2026, with 62% staked at a 2.9% annualized yield, and a deliberate decision to leave some ETH unstaked for liquidity. That is the moment Bit Digital stopped describing itself as a bitcoin miner and started describing itself as a treasury operator with optionality.

Behind those four publicly traded names is the queue. SBET and BMNR both joined the Russell 3000 in the 2026 reconstitution alongside Galaxy Digital, Gemini, IREN, and CoreWeave — a clear crypto-and-compute theme entering the broad-market benchmark. Private-round vehicles are pitching the same model to allocators every week. Lookonchain (@lookonchain) has documented multiple new wallet clusters consistent with corporate-style accumulation patterns beyond the named cohort.

The institutional plumbing is also forming around them. The spot-ETH retail rails at Charles Schwab and the regulatory stack that has fallen into place through 2026 are exactly the conditions that allow these vehicles to issue equity into public markets without friction. A year ago, the cohort could not have raised at this scale. Now it can.

Russell 1000 and the Forced-Buyer Mechanics

MicroStrategy's stock did what it did in 2024 partly because, after its Russell milestones, a wall of passive money had no choice but to own it. That dynamic is what BitMine is about to walk into — only earlier in its life cycle.

FTSE Russell published its preliminary additions list on May 22-23, 2026. BMNR is on it for the Russell 1000. The Russell 1000 inclusion threshold sits near a $5.7 billion market capitalization; BMNR comfortably clears that bar at roughly $10 billion. The final reconstitution closes by the end of June.

If finalized, the consequence is mechanical. The Russell US indexes serve as the benchmark for roughly $12T in assets. Index-tracking ETFs and pension mandates that follow Russell 1000 weightings will need to acquire BMNR in their respective weightings on the effective date. Active managers whose mandates restrict them to Russell 1000 names — and there are many — become eligible buyers for the first time. Tom Lee noted on X that passive funds and ETFs typically own 20-25% of any individual large-cap name's market cap over time.

That is a structurally different demand base than MicroStrategy enjoyed in 2021 or 2022, when the BTC treasury thesis was still dismissed as a curiosity. BitMine is being absorbed into the passive-flow apparatus near the beginning of its accumulation arc, not the end. And it will not be alone — every additional ETH treasury vehicle that clears the Russell 3000 threshold (SBET and BMNR already have) buys the cohort more permanent passive-buyer floor.

What Unwinds the Flywheel

The case is real. The risk is also real, and treasury bulls do themselves no favors by skipping past it.

The first vulnerability is the average cost basis. BitMine's disclosed average sits near $2,840. On-chain analyses from Lookonchain and several independent analysts, however, reconstruct the actual average closer to $3,997-$4,020 per ETH using on-chain flows from Kraken, FalconX, BitGo and known cluster wallets. With spot ETH around $2,100 as of this writing, the gap implies roughly $7-$8 billion of unrealized paper losses across the BitMine stack — even with the staking yield offsetting drag. Bit Digital's mark-to-market on its own treasury at $327M against a higher cost base tells the same story at smaller scale.

The second vulnerability is reflexivity, in reverse. The accumulation engine works only while the equity trades at a healthy premium to net asset value. If the NAV premium compresses — because ETH stays sideways, because dilution fatigue sets in, because the broader risk-on bid fades — the at-the-market issuance engine slows. Slower issuance means slower accumulation, which means slower premium support, which means slower issuance. The same flywheel runs the other direction.

The third vulnerability is concentration. BitMine alone owns more than 4% of circulating ETH. Add SBET, BTCS, Bit Digital and the private queue and a meaningful slice of ETH supply is now warehoused in a small number of public equity vehicles, much of it staked. That is a structurally different supply picture than 2021, and it could behave very differently in a stressed market.

The 2.9% staking yield does not eliminate any of these risks. It cushions them. It gives equity holders a recurring in-kind flow that compounds the ETH stack even when price action is unkind. That cushion is exactly what makes this wave look durable in a way the BTC treasury wave never quite did — but durable is not invincible.

Key Takeaways

- BitMine's 5.2M+ ETH treasury is the leading edge of a cohort that already includes SharpLink Gaming, BTCS and Bit Digital — and a queue of private-round vehicles behind them.

- The defining difference vs. the MSTR playbook is staking yield: roughly 4.36M of BitMine's ETH is staked, generating protocol-native rewards near a 2.9% annualized rate — giving the equity premium something resembling a cash flow underneath it.

- BMNR sits on the FTSE Russell preliminary list for Russell 1000 inclusion; final reconstitution closes by end of June 2026, layering on a forced passive-buyer base early MicroStrategy never had.

- Average cost basis is the load-bearing risk: analyst on-chain estimates put BitMine's true average near $4,000 ETH versus a $2,100 spot, implying billions in unrealized losses that the staking coupon cushions but does not erase.

- If the NAV premium compresses, the accumulation flywheel runs in reverse — but with a productive asset underneath, the compression looks materially less terminal than in the BTC-only model.

The Wider Lens. 2024 was the year the BTC treasury became respectable enough to issue equity into. 2026 is the year the ETH treasury becomes respectable enough to do the same thing — only with a yield component, a Russell inclusion path, and a cohort of operators rather than a single charismatic CEO. The bear case is the chart: average cost basis is well above spot, and a sideways ETH for a year would test how patient public-equity holders really are. The bull case is the math: a publicly traded vehicle that holds 4% of an L1's supply and earns protocol-native yield on three quarters of it is a financial primitive that did not exist twelve months ago. Watch the June Russell reconstitution, the next quarter of 8-K disclosures, and whether SBET's in-house staking desk produces yields that match BMNR's. That is where the thesis either gets confirmed or starts to crack.

Sources

Primary sources

- BitMine Immersion press release — 5.21M ETH, $13.4B total crypto and cash (PRNewswire)

- BitMine Immersion 8-K exhibit (SEC EDGAR, FY2026)

- SharpLink Gaming (SBET) 8-K — ETH treasury, in-house staking (SEC EDGAR)

- BTCS Inc. 8-K exhibit — Ethereum holdings disclosure (SEC EDGAR)

- Bit Digital — March 2026 Ethereum treasury and staking metrics

- FTSE Russell — 2026 US Indexes Reconstitution schedule (LSEG)

- Tom Lee — @fundstrat on X (BitMine chairman commentary)

- Lookonchain — @lookonchain on X (BMNR wallet tracking)

From BlockAI News

- BitMine's $126M, 60,000-ETH buy and the Russell index test (May 25, 2026)

- SpaceX's $1.29B bitcoin treasury disclosure in S-1 (May 25, 2026)

- Charles Schwab opens spot BTC/ETH retail trading (May 14, 2026)

- The institutional crypto regulatory stack falls into place (May 2026)

- Vitalik on AI formal verification for Ethereum security (May 19, 2026)

Stay close to the ETH treasury wave as it builds — quarter by quarter, 8-K by 8-K.

- Subscribe — the morning brief every weekday

- Telegram — every story the moment it ships

- @BlockAINews_ — short takes between issues

How we report: This article cites primary sources, regulatory filings, and on-chain data where available. BlockAI News uses AI tools to assist with research and first-draft generation; every article is reviewed and edited by a human editor before publication. Read our full How We Report page, Editorial Policy, AI Use Policy, and Corrections Policy.